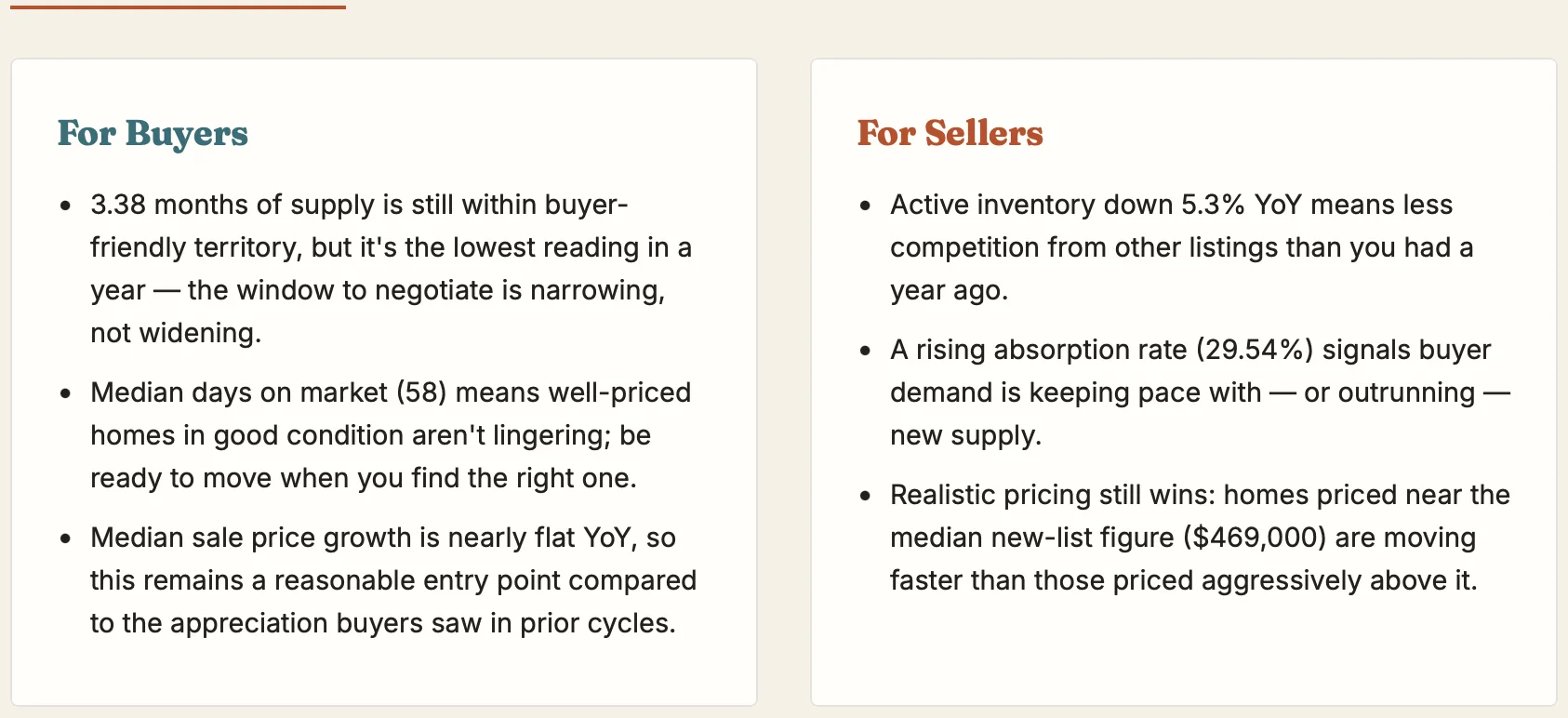

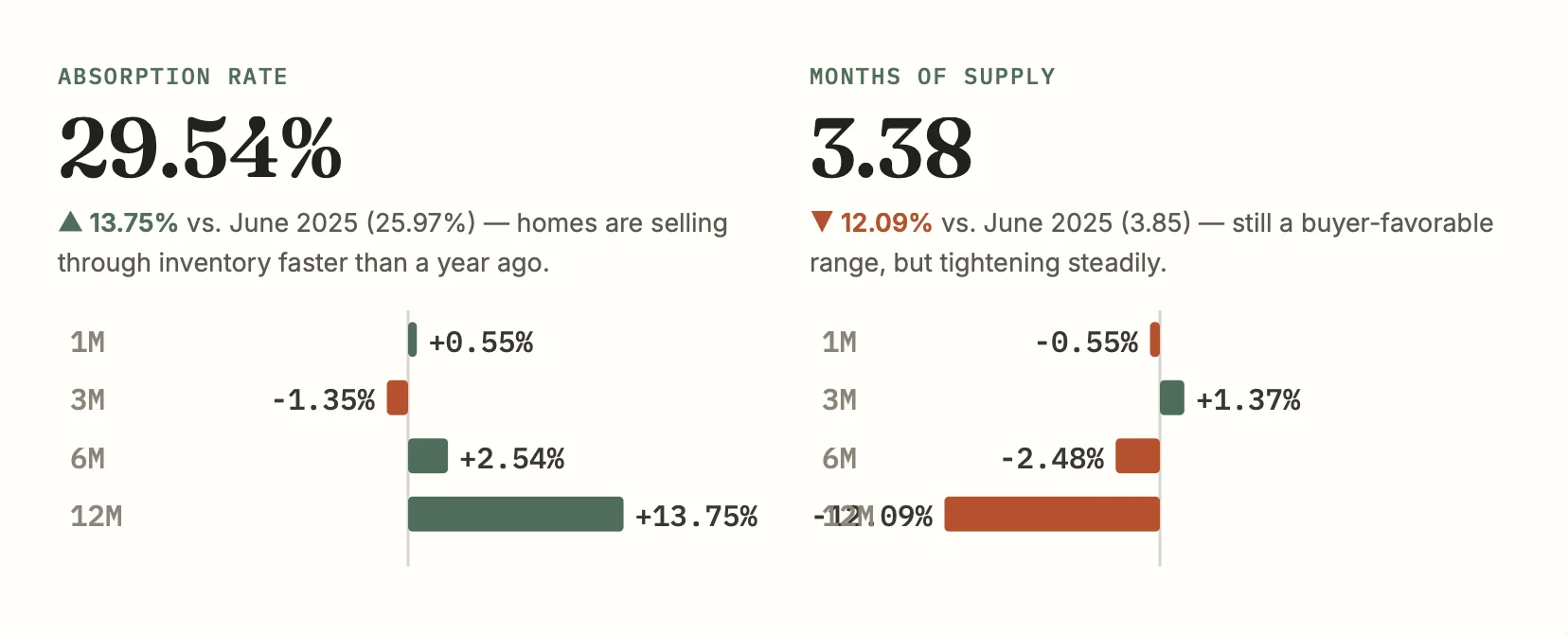

Months of supply measures how long it would take to sell current inventory at the current sales pace; absorption rate is the inverse view — the share of active inventory being sold each month.

Both metrics are telling the same story from opposite directions: supply is shrinking (3.38 months, down 12% YoY) and absorption is climbing (29.54%, up nearly 14% YoY). Anything under roughly 4-5 months of supply is generally considered favorable to sellers in most markets, and the Valley has now spent the better part of a year drifting toward that threshold rather than away from it.